Minimum pension drawdown not the only thing to consider as 30 June approaches

As 30 June approaches, SMSF members drawing a pension need to think about meeting minimum drawdown obligations as well as the best time to start a pension, an SMSF specialist said.

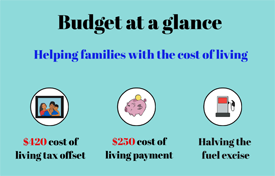

Key tax changes and measures from the 2026 Federal Budget

The major announcements from this year's Federal Budget and what they mean for accountants and their clients.

A breakdown of 2026-27 Federal Budget Themes and Papers.

. Global conflict has severely disrupted global oil supplies and is contributing to higher inflation, slower growth, and extreme economic uncertainty at home and abroad. At the same time, there are big structural changes unfolding in areas like energy and technology, and longstanding challenges when it comes to productivity, intergenerational equity and access to home

Federal budget 2026: Winners and losers

The Federal Government is selling the 2026-27 budget as a big reform budget. One that will tip the scales to make the tax system fairer for young Australians.

From Bricks to iPhones: The Evolution of the Telephone

Check out the history of communication, eventually leading to the modern phones we use today.

LRBA stability has been understated

The stability of limited recourse borrowing arrangements (LRBA) within SMSFs has been understated, with their track record highlighting their longevity and safety compared to other forms of property lending, a non-bank lender has stated.

Carer responsibilities don’t meet interdependency criteria: PBR

A parent who was the sole carer for a terminally ill child is not considered to be in an interdependency relationship, according to a private binding ruling.

Look for the red flags that signal unscrupulous advice

While the ATO is watching for signs of illegal early access to superannuation, SMSF trustees should also be on the lookout for red flags, a leading adviser said.

Magnificent Seven: More diverse than they may appear

The Magnificent Seven are more diverse businesses than their shared label suggests

Can I access my super early?

Many older Australians are understandably eager to access their superannuation, but strict rules apply

7 simple steps to get on the investment ladder

Entering the world of investing can be a life-changer for people of all ages. Here are seven simple steps for beginners to start their wealth journey.

SMSF commercial property owners and Div 296 ‘misconceptions’

There are three misconceptions among business owners with SMSF commercial property, a finance expert said

Rise in SMSF inflows indicate more people are moving into the sector

Inflows to SMSFs have almost quadrupled over the past five years and experts warn this trend warrants monitoring as it may signal shifting member preferences toward greater control.

View Division 296 as two-stage event

SMSF practitioners should view the pending Division 296 tax as rolling out in two stages, leading to two similar but different sets of rules in its first few years of operation, an SMSF sector specialist has noted.

Know the difference between death benefit pension and normal pension or pay the price

It’s vital to know what is and what is not a death benefit pension because the consequences of not paying the minimum pension payment on the wrong one could have dire consequences, a leading adviser said.

SMSF trustees acting badly – further disqualification cases

Several recent court decisions highlight the expectations of SMSF trustees in regard to legislative obligations.

In turbulent times, stick to your long-term wealth strategy

Why investors are urged to resist impulsive decisions in turbulent times

Most Valuable Industries in the World 2026

Check out which industries make up the biggest portion of the global ecomony.

Iran conflict: Keeping perspective on market risk

Tensions in the Middle East have rattled global markets. Both equities and bonds have experienced losses amid great uncertainty, and oil prices have spiked, creating a challenging dynamic.

Interest rates likely to stay higher for longer

The recent rate hike suggests that the Reserve Bank of Australia is prepared to move policy into more restrictive territory

Most Reliable Car Brands in 2026

Check out which car brands are the most likely to stay on the road and not cost you a fortune to fix.

AI use needed with proper safeguards

The SMSF Association has suggested practitioners servicing the sector must equip themselves with more than just technical knowledge in an era of rapid technological change to provide a robust advice proposition to clients.

Are downsizer contributions losing steam?

Tax Office data shows fewer people used its super scheme in 2024-25

Investment and economic outlook, February 2026

latest forecasts for investment returns and region-by-region economic outlook

Coercive control in SMSF becoming a hot issue

AFCA is anticipating there will be more focus on coercive control and elder abuse going forward.

What to look for when choosing a financial adviser

Here's how to find a financial adviser who can provide the right support for you

Thinking of establishing an SMSF? Don’t skip reading the rules

As the establishment of new SMSFs continues to rise, the ATO is reminding potential trustees to ensure they are aware of the different requirements depending on whether their fund has individual trustees or a corporate trustee.

Super versus trusts: What is the best option with Div 296?

Super used to be clearly the “best” option due to low tax rates but the increasing complexity of things like Division 296 tax, compliance risk, and death benefits tax is narrowing that advantage, a top specialist said.

Rare and vanishing: Animals That May Go Extinct Soon

Check out which animals are on the brink of extiction and If we don't act now, they could vanish forever.

Missed SG exemption may not be problem

Failing to exempt an employer from SG contributions may not be critical for some superannuants if it does not alter their tax position.

Don’t confuse contribution with roll-over when using proceeds from small business sale

Proceeds from the sale of small business using the 15-year CGT small business exemption is not a rollover to a superannuation fund, but rather a contribution.

ASIC warns investors on pump and dump scammers

How investors are being duped by unscrupulous operators

Australians not underspending their super

Drawdowns from super are now typically higher than the minimum amounts required, according to new research from the Super Members Council.

Investment and economic outlook, January 2026

The latest forecasts for investment returns and region-by-region economic outlook

ASIC targeting high-pressure sales and inappropriate advice

ASIC has highlighted that one of its main focus points in 2026 will again be high-pressure sales tactics and inappropriate financial advice.

Which country produces the most electricity annually?

Check out which Country Produce most Electricity per year (TWh), including Coal, Gas, Hydro, Nuclear, Wind, Solar, Oil and Bio.

What does 2026 look like in the SMSF sector?

Continued growth in the sector fueled by younger trustees looking at alternative investments are on the cards according to our experts.

It’s not just Div 296 that could face changes in 2026

With the objective of superannuation now firmly in place and a new draft of the Division 296 legislation out for consultation, it may seem there is little left to anticipate in the SMSF sector in 2026.

What had the biggest impact on the sector in 2025?

Looking back on 2025, there were several major changes that helped to re-shape the sector

Care needed with ceased legacy pensions

SMSF members with legacy pensions should be aware a commuted income stream may affect their Centrelink entitlements, but also the government has employed staff who can calculate the impact, a technical specialist has said.

Three timeless investing lessons from Warren Buffett

Warren Buffett is stepping back, but his investment wisdom endures

2026 outlook: Economic upside, stock market downside

AI’s rapid evolution has increased its potential to become a transformative economic force, with promising implications for productivity across industries.

Countries with the largest collection or eucalyptus trees

Check out the countries that have started to grow their eucalyptus tree stocks

Birth date impacts bring-forward NCCs

The provisions allowing SMSF members to trigger the NCC bring-forward rules in a subsequent financial year are birth-date sensitive.

12 financial tips for the festive season and year ahead

Some investing steps to get you through the holiday season, the new year, and for the future.

ATO issues warning about super schemes

The ATO is warning SMSF trustees to be on the look out for superannuation and tax schemes.

Move assets before death to avoid tax implications

Mitigating the impact of death benefit tax can be supported by ensuring the SMSF deed allows for the transfer of assets out of the fund in a timely manner, a legal specialist said.

Investment and economic outlook, November 2025

The latest forecasts for investment returns and region-by-region economic outlook

Becoming a member of an SMSF is easy, but there are other things that need to be considered

There are very few restrictions on who can become a member of an SMSF, but there are conditions with which members must comply when they are in a fund, a specialist adviser said.

AI exuberance: Economic upside, stock market downside

The key findings of Vanguard’s economic and market outlook to be released in December

How Many Countries Divided From The Largest Empire throughout history

Check out the countries that have been born from some of the largest empires in history.

Call for SMSF ‘nudge’ in DBFO package

The peak SMSF body has called on the government to extend the member ‘nudge’ rules beyond industry and retail super funds.

Beware pushy sales tactics targeting your super

The Australian Securities and Investments Commission (ASIC) has warned Australians to beware of high-pressure sales tactics aimed at getting people to switch superannuation providers.

Determining what is an in-house asset can help determine investment strategy

It is important to understand what is and what isn’t an in-house asset to ensure compliance in an SMSF, a leading technical specialist has said.

Stress-test SMSF in preparation for Div 296

SMSFs that hold farms or small businesses should do a “stress test” on their funds in preparation for the Division 296 tax, a leading adviser has said.

Investment and economic outlook, October 2025

Latest forecasts for investment returns and region-by-region economic outlook

Accountants united in support for changes

The three major accounting bodies have backed the changes to the Division 296 tax and have called for it to be implemented quickly.

How to budget using the envelope method

Here's five simple steps to create a budget that doesn't involve tracking every expense

Airplane Fuel Consumption Per Minute

Check out the fuel consumption per minute of different airplanes — from small propeller planes to giant airliners and powerful fighter jets.

New NALE guidance still has issues

The ATO has released its updated Law Companion Ruling (LCR) 2021/2 regarding the application of non-arm’s length income (NALI) laws with the SMSF Association giving it a mixed welcome noting it still lacks specific guidance in places.

Younger Australians expect more for their retirement

Australians under 45 now expect they will need at least $100,000 a year per household to live comfortably in retirement, according to new research from Vanguard.

Evolution of ‘ageless workers’ sees retirement age rise

Australians are retiring later due to cost-of-living pressures and the evolution of white-collar employment, according to research from KPMG.

Caution needed if moving assets to children

Legal advisers need to be cautious when transferring assets from parents to children if the former are still alive.

Investment and economic outlook, September 2025

Latest forecasts for investment returns and region-by-region economic outlook

Five building blocks that could lead to a more confident retirement

How Australia Retires 2025 report, explores how Australians prepare for and experienced retirement.

How changes to deeming rates could affect your pension payments

What the end to the deeming freeze means for Age Pensioners

The biggest earthquakes in history : (1905–2025)

Check out this powerful visual journey through the most powerful earthquakes ever recorded. From massive Chilean earthquakes along the Pacific Ring of Fire to the more recent Russia earthquake in Kamchatka, this timelapse shows how Earth's fury has shaped our world.

Compassionate release warning issued

The ATO has warned consumers, financial advisers and health practitioners it is aware of dishonest practices being used to access superannuation early for non-critical medical procedures.

ATO warns that SAR lodgments are on its radar

Outstanding SMSF annual returns will be a primary focus of the ATO, the deputy commissioner has said.

How ‘investment procrastination’ could be hurting your wealth

Putting off investing could cost you more than you think.

New report highlights confusion over BDBNs

Less than a quarter of Australians have made valid binding death benefit nominations, new research has shown.

investment and economic outlook, August 2025

latest forecasts for investment returns and region-by-region economic outlook

Common sense the best defence against fraudsters: forensic auditor

Basic common sense is one of the best tools to detect fraudulent schemes, a forensic auditor has said.

How $1,000 plus regular contributions turned into $823,000 through compounding

A simple ongoing investment strategy can deliver substantial returns over time

The rise and fall of the world’s largest economies | GDP Epic Battle (1560–2025)

From the age of empires to modern global superpowers, check out the rise and fall of the worlds superpowers.

Avoid LRBA structure short cuts

SMSF trustees using limited recourse borrowing arrangements (LRBA) should avoid trying to cut corners in setting up a trust for the loan, with an SMSF structure expert stating they should set up a dedicated bare trust for each gearing measure.

Challenges with TBC increase for those in pension phase

The increase in the transfer balance cap from $1.9 million to $2 million is not as simple as it seems, particularly for members already in pension phase, a leading adviser has said.

Death benefits not reliant on probate

A retirement savings specialist has confirmed the payment of an SMSF death benefit is not dependent upon any of the procedures associated with the deceased member’s estate.

ATO flags October SAR lodgment date

The Tax Office has reminded trustees that SMSFs need to start preparing for their SMSF annual return lodgment, which is due by 31 October 2025.

Investment and economic outlook, July 2025

Latest forecasts for investment returns and region-by-region economic outlook

How personal data could boost your retirement income by up to 50%

Tailoring your retirement strategy based on your personal data could be invaluable

How financial advice can reduce stress and save time

Research explores the benefits investors can derive from financial advice

How topping up your super each year could leave you $80,000 better off in retirement

The power of regular voluntary super contributions

A super contributions deadline you won’t want to miss

If you plan to get more into your super this financial year, act very quickly.

Leasing property owned by an SMSF

The rules for a super fund investing in property are complex because of the restrictions placed on some types of property that may be acquired (purchased or transferred in specie) from related parties.

Beware of tax implications for failing to meet minimum pension requirements: consultant

Failing to meet the minimum pension requirements impacts a number of tax components, an industry consultant has warned.

Roles and Responsibilities in a Business Partnership

Set clear expectations from the start of your partnership

ATO warns SMSF trustees to be aware of increase in scams

The ATO has issued a warning to SMSF trustees to be aware of scammers leading up to EOFY.

Div 296 sparking death benefit discussions

The Division 296 impost has prompted SMSF members looking at retaining assets in super to consider the tax impact of their death on their beneficiaries.

Comparison of various Animal Weight

Check out the lightest to heaviest animals in the world

New SMSF trustees propel uptake of financial advice

The $1 trillion superannuation sector still has significant advice gaps

Start-ups to suffer under Div 296

The head of a prominent funds management house has predicted the proposed Division 296 tax will significantly diminish the supply of critical capital required for start-up companies as many of these enterprises rely on SMSFs for funding.

Your 30 June superannuation checklist

With the end of the current financial year fast approaching, time is running out if you’re planning to boost your superannuation balance before 30 June.

Legal case has succession planning lessons for SMSF members, advisers: legal expert

The recent Federal Court case, Lynn v Australian Financial Complaints Authority [2025] FCA 175, has highlighted the importance of clear succession and estate planning to ensure a deceased member’s super death benefits are paid as intended, a legal specialist has said.

Investment and economic outlook, May 2025

Tariff reprieves, trade deals brighten the economic horizon

ASIC to increase audit surveillance in 2025–26

The corporate regulator has said it will review an increased number of audit files in the upcoming financial year.

ATO issues guidance on SMSF trustee appointment and compliance

The ATO has issued guidance on what SMSF members need to understand about compliance regarding responsibilities when appointing trustees or directors of a corporate trustee.

Freshwater Resources by Country 2025

Check out the largest freshwater resources by Country in the World

Financial abuse move now a certainty

Bipartisan support now exists to prevent perpetrators of financial abuse and domestic violence from accessing the victim’s superannuation benefits upon their death after the Coalition pledged to take this action should it win power at the federal election in May.

Are your adult children ready for the wealth transfer?

The inheritance wave is building but most people are unprepared for the ride

How boosting your super can help you reduce your tax bill

Here's how topping up your super can help reduce your tax bill

Trustees reminded of minimum pension drawdown

The ATO has reminded trustees they have until 30 June to make their minimum payment from their pension.

Investment and economic outlook, April 2025

The latest forecasts for investment returns and region-by-region economic outlook

Why more Australian SMSF owners are looking to global equities

Australian SMSFs have historically maintained strong exposure to local assets, with portfolios concentrated in Australian shares and cash.

$95bn loss predicted to Australian economy if Div 296 passes: analysis

Analysis from one of the country’s biggest asset management firms has revealed a “deadweight loss” of $94.5 billion to the nation’s economy if the Division 296 tax gets over the line.

The Largest Empires in the World’s History

Check out the Largest Empires in the World's History

Trustees warned on early access

The ATO has warned trustees they will be held accountable for members who access super without meeting a legitimate condition of release.

SMSFs hold record levels of cash and property

SMSFs are holding record levels of cash despite an interest level drop in February, according to ATO data.

Advisers should be aware of signs of elder abuse in SMSF structures

SMSFs are a structure that can heighten and exacerbate issues around elder abuse, a leader in the aged care sector has said.

Investment and economic outlook, March 2025

latest forecasts for investment returns and region-by-region economic outlook

The Most Held Currencies in the World | 1850-2024

Check out the most powerful Currencies in the World | 1850-2024

Building Australia’s future and Budget Priorities

Building Australia's future and Budget Priorities

All the documents, fact sheets and downloads to do with this year’s 2025-26 Federal Budget

Federal Budget 2025-26 – Papers and Fact Sheets

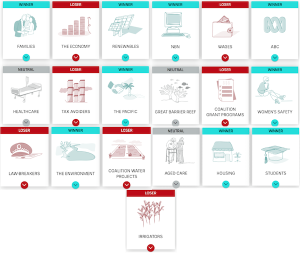

Winners and Losers – Federal Budget 2025-26

Treasurer Jim Chalmers has handed down his fourth federal budget, laying the groundwork for a federal election campaign that could be called within days.

Retiree confidence undermined

Cost-of-living pressures have eroded retiree confidence and prompted many to recalibrate their expectations, according to a new financial services sector report.

Increase in prohibited loans a concern: ATO

While the amount of illegally accessed funds from SMSFs has reduced, the amount of prohibited loans has gone up, the Commissioner of Taxation has said.

SAR non-lodgment continues to be a concern: ATO

The non-lodgment of superannuation annual returns continues to be one of the ATO’s major concerns, the deputy commissioner for superannuation has said.

TBC increase not just about pensions

An industry consultant has reminded practitioners the indexation measure to be applied to the general transfer balance cap will have implications for other elements of the superannuation system as well that are unrelated to income streams.

Investment and economic outlook, February 2025

The latest forecasts for investment returns and region-by-region economic outlook.

Home is where the super is for many Australians

More Australians are upsizing their super by downsizing their home.

Four SMSF breaches high on the ATO’s radar

The Tax Office is actively targeting SMSF trustees over a range of super breaches. Home ownership is still the great Australian dream for many people.

How to shift into pension mode

When and how you can access your super to start an account-based pension.

Five financial steps for the new year

The start of 2025 is a good opportunity to take decisive financial steps.

Division 296 deliberately deceptive

A senior financial services industry executive has labelled the Division 296 tax as political deception, seeing there has been no honest indication of who the impost will really affect.

Carer rights – interdependency relationships

The stringent rules applied to the definition of interdependency have again been highlighted in a recent private binding ruling.

Australia’s economic growth set to recover in 2025

GDP growth is set to gain momentum despite sticky inflation and high interest rates.

Calls for clarification on NALI/E rulings

The ATO needs to provide clarification on a number of issues in the law companion ruling dealing with NALI/E, the joint bodies have said.

Up to 700k retirees could be paying more tax than they should: SMC

Lack of proper financial advice is costing hundreds of thousands of retirees in unnecessary taxes, the Super Members Council has said.

Most Powerful Economies in Europe | 1960-2024

Check out the most Powerful Economies in Europe | 1960-2024

End-of-year break time for super check-up

Superannuants should use the end-of-year holiday break to check the status of their retirement savings and consider if advice would be useful to them, given many are unsure how much they will need at the end of their working life, an industry body has stated.

9 Ways You Can Invest Using SMSF

Review nine smart ways to invest using an SMSF, from property and international shares to cryptocurrency and managed funds. Maximise your retirement savings wisely.

Super funds finish 2024 with double-digit returns

Most superannuation funds finished 2024 with double-digit returns, according to a recent analysis.

Know the difference between general and specific NALE

SMSF professionals should take note of the wording changes in Law Companion Ruling 2021/2DC, which outline the differences between specific and general NALE, a legal specialist has said.

It’s super hump month. Make the most of it

The start of the 2024-25 financial year on 1 July saw some significant changes come through designed to help working Australians get more money into their superannuation.

Investment and economic outlook

latest forecasts for investment returns and region-by-region economic outlook.

Top 20 Most Watched Christmas Movies ever – pre covid

Check out the top 20 Most Watched Christmas Movies ever – pre covid

$3m super tax officially abandoned for this year

The government’s plan to increase the tax on superannuation balances over $3 million has officially been abandoned, at least for this year.

Divorce doesn’t alter contribution rules

The Administrative Appeals Tribunal (AAT) has upheld an ATO decision to impose an excess contributions penalty and rejected a taxpayer’s claim a divorce-related superannuation split constituted special circumstances under taxation law.

Navigating the outcome of the U.S. election

History suggests that investors shouldn’t be concerned about material asset return differences under different political administrations.

How to overcome your investment fears

Are you thinking of investing but feel held back? Here's how to get started.

Preparing to lodge quarterly January TBAR

The ATO is reminding SMSF trustees that if they have had transfer balance account events in the last quarter they must lodge a TBAR by 28 January 2025.

Economic and market outlook for 2025: Global summary

The global outlook summary highlights the top-level economic and market outlook, Beyond the landing, to be distributed in mid-December.

Women still outpacing men in SMSF establishments

More women than men entered into SMSFs in the September quarter, according to the latest ATO statistics.

A Unique Advent Calendar

Once again we are pleased to release an advent calendar. One developed especially for you, our clients, your family and your friends. Come back each day and click on the next date for more inspirational and Christmas quotes. We can't be sure but it seems this year has gone faster than any year previously, we

20 Years of Silicon Valley Trends: 2004 – 2024 Insights

Check out the 20 years of Silicon Valley Trends

The biggest assets growth areas for SMSFs

What five years’ worth of SMSF asset allocation data reveals.

Caregiving can have a retirement sting

Around 3 million Australians are unpaid caregivers. Most face a super risk.

Be clear on TBA pension impact

The different operations of pensions passed onto a beneficiary can be confusing and SMSF members must understand how the will impact their transfer balance account.

Leaving super to an estate makes more tax sense, says expert

It is more tax effective to leave superannuation to an estate rather than a binding death benefit nomination to children, says an accounting expert.

Investment and economic outlook, October 2024

The latest forecasts for investment returns and region-by-region economic outlook.

Compliance documents crucial for SMSFs

Failure to create, execute, perform and retain documents for an SMSF can leave a fund and its trustees unable to provide compliance evidence, warns a specialist legal expert.

ATO reviewing all new SMSF registrations to stop illegal early access

The ATO said it is reviewing and assessing all new SMSFs before they can receive a registered or complying status on Super Fund Lookup (SFLU) as part of a program to stop illegal early access schemes.

The Leaders Who Refused to Step Down 1939 – 2024

Check out the The Leaders Who Refused to Step Down 1939 – 2024

ASIC extends reportable situations relief and personal advice record-keeping requirements

ASIC has extended the reportable situations relief and personal advice record-keeping requirements on the same terms until October 2029.

Age pension fails to meet retirement needs

New research has found most Australians believe the age pension is insufficient to fund their retirements, with larger superannuation balances and access to professional financial advice linked to higher levels of financial well-being instead.

A new day for Federal Reserve policy

What the Federal Reserve's policy shift means for rates.

What are the government’s intentions with negative gearing?

Both the Treasurer and the Prime Minister have confirmed that Treasury is exploring changes to the contentious policy.

ATO stats show continued growth in SMSF sector

The ATO’s June quarterly statistical data on the SMSF sector has been released and has revealed continued growth.

Economic slowdown drives mixed reporting season

Many Australian companies are still battling economic crosswinds and headwinds.

Investment and economic outlook, September 2024

The latest forecasts for investment returns and region-by-region economic outlook.

SMSF succession planning part 1 – getting started

Part 1 examines the key characteristics of a sound SMSF succession plan including planning for control of the fund to pass into trusted hands in the event of a member’s death or loss of capacity.

Most Popular Operating Systems 1999 – 2022

Check out the most Popular Operating Systems 1999 – 2022

Super sector in ASIC’s sights

The superannuation sector’s handling of retirement outcomes will be an area of focus for ASIC which has also committed to review SMSF establishment advice.

How investing regularly can propel your returns

Even investing small amounts on a regular basis will compound returns over time.

What the Reserve Bank’s rates stance means for property borrowers

The funding gap between variable and fixed rate loans is continuing to widen.

Investment and economic outlook, August 2024

Region-by-region economic outlook and latest forecasts for investment returns.

Capital losses can help reduce NALI

Capital losses can be used to reduce or eliminate NALI tax exposures in relation to a tainted capital gain, says a legal expert.

Beware of terminal illness payout time frame

If an SMSF member is diagnosed with a terminal illness, it is best not to close out the fund before the insurance has been paid, says a specialist.

ATO encourages trustees to use voluntary disclosure service

The ATO is encouraging SMSF trustees to use its voluntary disclosure service to inform it early if a contravention has occurred.

Treasurer unveils design details for payday super

The government has released further details about the design of its payday super policy including an updated super guarantee charge framework.

Government releases details on luxury car tax changes

The draft legislation aims to modernise the luxury car tax by tightening the definition of a fuel-efficient vehicle and adjusting the indexation rate.

Most Gold Medals in Summer Olympic Games (1896-2024)

Check out which country has won the most Gold Medals in Summer Olympic Games (1896-2024)

Capacity doubts now more common

The partner of a legal firm specialising in superannuation has revealed the concept of SMSF member mental capacity is becoming more prevalent in estate planning challenges, prompting the need for practitioners to amend their procedures regarding all fund actions.

It’s never too early to start talking about aged care with clients

Financial planning professionals should be having conversations with their clients as soon as possible about their aged care needs, says a specialist adviser.

Warning to micro businesses. ‘Higher taxes for thousands of businesses’.

The ATO’s draft guidance on personal service income and the general anti-avoidance provisions is likely to be a shock to many small and microbusinesses in Australia.

COVID early super release did little for financial, emotional wellbeing.

The Early Release of Super scheme implemented during the COVID-19 pandemic had little impact on financial resilience or wellbeing, new research has shown.

Insurance inside super has tax advantages

One of the most significant advantages of holding insurance policies inside superannuation is the tax deduction for life and disability premiums that go towards paying out a disability superannuation benefit, according to a leading technical specialist.

What super fund members should know when comparing returns

Why you need to compare apples with apples on super fund performances and fees.

The five reasons why the $A is likely to rise further – if recession is avoided

After a soft patch since 2021, there is good reason to expect the $A to rise into next year

Taxing unrealised gains in superannuation under Division 296

Australia’s superannuation system has seen a number of significant changes in recent years.

Striking a balance in the new financial year

By doing a few calculations you can easily see if your portfolio is still on track.

Our investment and economic outlook, July 2024

Our region-by-region economic outlook and latest forecasts for investment returns.

Income-free areas set to increase from 1 July

People nearing retirement often want to know how much they can earn before it affects their pension, and now there is a bit of good news on the horizon for SMSF members who receive the Age Pension.

LRBA interest rates increase for 2025

The safe harbour interest rate for related party limited recourse borrowing has changed for 2025.

Compliance focus impacts wind-ups

The ATO’s strategic increased focus on compliance is having a noticeable effect on the sector and is now the most common reason why many SMSF trustees have closed their funds, the latest Investment Trends research has shown.

NALE bill passed by parliament

The bill that will introduce changes to the non-arm’s-length expenditure (NALE) provisions has passed through parliament and is now awaiting royal assent before it can take effect, possibly as early as 1 July.

How to get into the retirement comfort zone

A third of Australians retire without a plan. Here's why you should have one.

Many Australians have a fear of running out

Longevity risk is a growing concern for many working Australians as well as retirees.

SMSF assets reach record levels amid share market rally

How SMSF trustees are investing their retirement savings.

The superannuation changes from 1 July

The super changes on the way from the start of the 2024-25 financial year.

Downsizer contributions can be time critical

With the expansion of the downsizer contribution, the timing of when it is used can affect how to use non-concessional contributions.

Deeming freeze a win for Age Pensioners

Why the decision to keep deeming rates on hold may be a window for interest rates.

Plan now to take advantage of stage 3 tax cuts

With the stage three tax cuts set to be implemented in around six weeks, opportunities for tax-saving strategies should be considered soon.

Investment and economic outlook, May 2024

Region-by-region economic outlook and latest forecasts for investment returns.

Middle-to-higher incomes boosting SMSF growth

The SMSF sector experienced healthy growth over the March quarter, with men and women on middle-to-higher incomes driving an increase in new funds established, according to statistics released by the ATO.

ATO warns trustees about increasing crypto scams

SMSF trustees are being warned to be on the lookout for crypto investment scams.

The Shortest-reigning Monarchs in History

Check out the Shortest-reigning Monarchs in History

ACCC scam report

Australians made more than 600,000 reports about scams in 2023 — about 18 per cent more than in 2022.(ABC News: Evan Young/Canva)

Connecting an adviser with your children

How parents and advisers can work together to manage intergenerational wealth transfers.

Australia’s debt service ratio ‘extraordinary’: CBA

The change in the debt service ratio has been ‘extraordinary’, according to the major bank.

Federal Budget 2024

Four main components of this year's Federal Budget can be seen by using the following links.

Winners & Losers

Jim Chalmers has handed down the government's third budget, with a $300 power bill boon for every Australian household, but the purse strings kept tight on other measures.

Budget breakdown – Federal Government Analysis

The 2024 Federal Budget is broken down into these five PDFs. Click on each to read more.

Investment and economic outlook, April 2024

Our region-by-region economic outlook and latest forecasts for investment returns.

What is the future of advice and how far off is superannuation 2.0?

Financial advice can make a massive difference in people’s lives. We know this because we see every day in our data just how much better off people are when they follow the advice. But up until now, the majority of Australians haven’t been able to afford it. As a consequence, most Aussies are unaware of what advice is and how it can help them be better off.

Getting to a higher level of financial literacy in Australia

The practical benefits of improving financial literacy.

The compounding benefits from reinvesting dividends

Using income distributions to purchase additional ETF units can significantly compound capital growth and income returns over time.

Investment and economic outlook, March 2024

Region-by-region economic outlook and latest forecasts for investment returns.

The 2025 Financial Year Tax & Super Changes You Need to Know!

The new financial year is fast approaching and so are a number of changes to superannuation contribution amounts and the individual tax rates. These changes are outlined below, as is some information on how you may be able to work with these changes when managing your tax affairs during 2024-25.

ATO investigating 16.5k SMSFs over valuation compliance

More than 16,500 SMSFs are being scrutinised by the ATO as they allegedly reported certain classes of assets at the same value for at least three income years.

Removed super no longer protected from creditors: court

A recent Federal Court ruling has found that the transfer of super from a husband to his wife’s superannuation account is no longer protected as an interest of the bankrupt in a regulated super fund under the Bankruptcy Act 1966.

Aged care report goes to the heart of Australia’s tax debate

The Aged Care Taskforce was asked to report on how to fund aged care around the country. In so doing, it took a side in Australia’s national tax ‘tragedy.’

Countries producing the most solar power by gigawatt hours

Check out the countries that produce the most solar power.

Could your SMSF do with more diversification?

Australian Tax Office Office data shows a high percentage of SMSFs are lacking portfolio diversification.

Planning financially for a career break

A pause in super contributions can have long-lasting effects. Here's how to plan ahead for super breaks.

Investment and economic outlook, February 2024

Region-by-region economic outlook and latest forecasts for investment returns.

Latest stats back up research into SMSF longevity and returns: educator

There was a dramatic decrease in the number of SMSF wind-ups from 2018 to 2023, indicating that the SMSF sector is outperforming APRA funds in both returns and customer satisfaction, says a leading educator.

Regular reviews and safekeeping of documents vital: expert

Keeping track of all documents relating to an SMSF trust deed is important if an estate planning issue arises, says an industry expert.

Trustee decisions are at their own discretion: expert

A trustee doesn’t need to show reasons why they made a decision, they will only need to show they followed a proper decision-making process, says a specialist legal adviser.

Illegal access nets $637 million

The ATO has found $637 million of superannuation savings has left the system due to illegal early access carried out through SMSFs.

Investment and economic outlook, January 2024

Region-by-region economic outlook and latest forecasts for investment returns.

Four timeless principles for investing success

Investing success can mean different things to different people. Being clear on what success means for you is key to mapping out your plan.

Super literacy low for cash-strapped

Financial literacy around superannuation is poor for many lower-income people, who still question why they can’t access their funds until retirement age.

Why investors are firmly focused on interest rates

2024 is very much a story of how quickly and how sharply rates will start coming down.

Plan now to take advantage of 5-year carry forward rule: expert

This is the last year that the five-year catch-up contribution rules for concessional contributions can be used for those who are eligible, warns a leading educator.

Quarterly reporting regime means communication now paramount: expert

Communication between SMSF trustees, accountants and advisers is more crucial than ever with the quarterly reporting rules coming into force, says a leading specialist.

Labor tweaks stage 3 tax cuts to make room for ‘middle Australia’

Following years of mixed messaging, Labor has bowed to economic pressure and announced changes to its stage three tax cuts.

Tips for preparing for the best tax outcomes

In the final of our series of predictions for the coming year, we asked our experts what trustees should be considering regarding tax savings in 2024.

The Countries that Export the Most Wine in the World

Check out the countries that export the most wine in the world

How to tame the market’s skewness

Outperforming the market is hard without a crystal ball. Here's how to tilt the odds in your favour.

Why crypto treads an uncertain path through tax minefield

The taxation of digital assets used for lending and borrowing would benefit from clear-sighted guidelines.

An investment year of ups and downs

How and why investment markets have performed the way they have this year.

Vanguard economic and market outlook for 2024: A return to sound money

Our economic and market outlook for 2024 reflects the house view of Vanguard’s global economics and markets teams as of December 12, 2023.

Millions of Australians lose by leaving savings in default MySuper funds

More than 5.2 million young Australians are missing out on higher superannuation returns by investing their retirement savings in default MySuper accounts, according to research from Innova Asset Management.

Time to start planning for stage 3 tax cuts: technical manager

Advisers should start planning how to take advantage of the stage three tax cuts due to come into force next year, says a leading technical expert.

Most Expensive Wars In History

Check out the most most expensive wars throughout history

Setting up the next generations of retirees

With average life expectancies rising, early investment education and financial advice will become increasingly critical.

Economic and market outlook for 2024: Global summary

The global outlook summary highlights the top-level findings of the full economic market outlook.

EPOA crucial for SMSFs, says professional adviser

An enduring power of attorney is crucial for ensuring continuity and compliance, says a professional adviser.

Does the NALI/E punishment fit the crime?

The long-running NALI/E debate has not considered the “extremely heavy-handed treatment” the specific asset NALI provisions impose.

A 2023 Advent Calendar for our clients

Come back each day and click on the next date for more inspirational and Christmas quotes.

Retirement is not just about dollars

A life-cycle consultant has revealed only two in five retirees admit to being happier once they stopped working, prompting him to issue a reminder that achieving a satisfactory retirement goes well beyond how much money a person has saved in their superannuation fund.

Most powerful countries throughout time.

Check out the most powerful countries in every century.

Teaching children about the value of money

Transferring money to children can be one of the most valuable financial steps parents can take.

Investment and economic outlook, October 2023

The peak drag on consumption caused by European Central Bank (ECB) monetary policy will likely occur in the first two quarters of 2024, according to Vanguard research.

SMSFA says proposed super legislation will hit farmers, small businesses the most

Small business owners and farmers with land or business premises owned by their SMSF are the big losers in the draft legislation on the Better Targeted Superannuation Concession, claims the SMSFA.

How to budget using the 50/30/20 method

This is a great strategy for anyone who wants an easy and structured budgeting method.

ATO takes hard line on in-house asset rules

A recent announcement from the ATO on in-house asset rules has left many in the auditing sector stunned, claims a leading adviser.

Working after pension age

The Australian Government is assisting older Australians to work, if they are able and wish to do so, by allowing them to keep more of their pension when they have income from work.

Big stamp duty and tax changes for Victoria investors and businesses.

There are three main areas of significant change: Transition from stamp duty to annual property tax for commercial and industrial property. This will apply to commercial and industrial properties acquired on or after 1 July 2024. (existing owners of properties purchased before 1 July 2024 will not be affected). Once a property enters the

High deposit rates, but the case for equities is strong

Investors can currently lock in attractive term deposit rates, however equities are still likely to outperform cash over the longer term.

Revised NALE rules ‘miss chance to clarify SMSF bugbear

The ATO will need to help trustees work out when an arrangement is internal to the fund for the purposes of non-arm’s length expense rules, says the NTAA.

Our investment and economic outlook, September 2023

Read our region-by-region economic outlook and latest forecasts for investment returns.

6 simple rules will ensure a deed can be executed in all states

There are six simple rules that will ensure a deed is executed properly in every Australian state, says a leading superannuation legal consultant.

The benefits and risks of collectable super assets

While owning collectable and personal use assets inside a SMSF may sound appealing, there’s a big catch.

Too many businesses roll the dice on tax debt: Jordan

Profitable companies that choose to relegate their tax and super obligations will be a focus of the ATO’s crackdown on collectable debt, Commissioner says.

Unfair Terms in a Standard Form Contract

As a business owner, you probably enter into contracts every day. Contracts are crucial as they document and govern the relationship between your business and various parties. It is common to offer the parties you interact with the same or similar contracts. These are examples of a standard form contract.

Oldest Buildings in the World

Check out the oldest buildings in the history of the world.

Super gender divide to remain a challenge

The Federal Government has flagged it expects the gender gap in superannuation balances to persist well into the future.

Last chance for $25,000 super deduction

For those with a super balance under $500,000, the 2024 financial year is the final year unused concessional contributions from the 2019 financial year can be applied.

Managing complex relationships in SMSFs comes down to well-crafted deeds

Marriage breakdowns and SMSFs are tricky and expensive, but if the fund has extended family members included it can get even trickier, says the head of a national SMSF advice company.

Our investment and economic outlook, August 2023

Read our latest forecasts for investment returns and our region-by-region economic outlook.

Transferring wealth to the next generation

Inheritance planning, particularly the future division of wealth and the intended treatment of assets, should be openly discussed at the family level.

Single-asset segregation barred

A single asset cannot be treated in a manner that allows it to support some SMSF members in accumulation phase and others with a pension account.

The top mode of transport in the world

check out the top modes of transport and how prevalent they are.

Returns rebound in 2022-23

Investment markets rebounded in 2022-23. But it's important to understand that asset class returns vary from year to year.

Understanding the role of custodians

Investment custodians have an important function to safeguard the assets of millions of Australian investors.

Our investment and economic outlook, July 2023

Read our latest forecasts for investment returns and our region-by-region economic outlook.

Taxing unrealised capital gains a grave concern: Burgess

The SMSFA has renewed its call for a more equitable and less costly approach to the federal government’s proposed new tax on superannuation balances exceeding $3 million.

From purchase to lease, SMSF property documentation is essential

Lease agreements for property must also adhere to non-arm’s length regulations to avoid the scrutiny of the ATO, says an SMSF expert.

Living comfortably in retirement just got more expensive

The amount of superannuation needed to live comfortably has risen to a record high as the cost-of-living crisis continues to impact all Australians.

SMSFs will continue to grow as government eyes superannuation coffers

Following the release of the government’s latest Intergeneration Report there is renewed confidence that more people will see SMSFs as a more attractive option as a savings vehicle for retirement.

Advice-Related Complaints Low Despite Huge Rise In General

Of the nearly 97,000 complaints lodged with AFCA in the past 12 months, less than 5% were related to investments and advice and just under 2% were about life insurance.

A statement from the authority says consumers in dispute with financial firms lodged a record 96,987 complaints, an “unprecedented” rise of 34% on the previous financial year.

Average ATO refund tumbles $430 compared to last July

Fewer taxpayers have raced to file an early return and the total paid out in refunds is already down by $1.7 billion.

Penalty amnesty tempts 7,000 small businesses back into tax system

UPDATED: This budget measure waives fines for late lodgment of income, BAS and FBT returns due during the pandemic.

More Australians are unlocking home equity to fund retirement

A growing number of Australians are downsizing their home to fund their retirement. Here's the latest data from the ATO on use of the downsizer measure.

The “secret” to financial freedom? Persist while others quit

See what it means to persist in the face of market volatility.

Australians need a retirement confidence boost

Giving Australians better access to high-quality and more affordable financial advice is imperative.

High interest and inflation can pay dividends for SMSFs

While much of investors’ attention is naturally aimed towards the impact on mortgage repayments, higher rates are opening massive opportunities for retirees in term deposits, bonds and lower-risk assets, says the director of a leading wealth management firm.

Five questions that indicate how financial literate you are.

Australia has a relatively high level of financial literacy when ranked globally. In

a study of 140 economies, Australia ranked in the top 10 countries for financial

literacy.

Tax alert warning could catch more in the ATO web

It’s not just SMSF trustees that may be caught under the tax alert issued last week in regards to property and arms’ length dealings, warns a specialist SMSF legal expert.

Top 50 Greatest Inventions in History

Check out the greatest inventions in human history!!!

The strong link between advice and retirement confidence

Seeking professional advice could lead to greater confidence in being financially prepared for retirement.

The keys to high retirement confidence

Are you retirement ready? Our inaugural How Australia Retires study has uncovered some common themes that make Australians highly confident about their retirement.

Banking on the Age Pension

The ranks of Australians receiving the Age Pension are increasing. It’s important to understand who is eligible and its role in retirement planning.

Inflation drives the cost of retirement to a record high

Self-funded retirees are the hardest hit by the increasing rise in inflation and cost-of-living according to the latest research from Association of Super Funds Australia.

Legislation changes give market-linked pensions better outcome

There is now more flexibility for SMSF members with market-linked pensions whose balances exceed the transfer balance cap with better tax outcomes and estate-planning options said the managing director of a leading SMSF educational organisation.

Summary of Superannuation Issues and Recent Changes

Recent Issues and changes that could effect you

Australians Seek Financial Independence – Report

The priorities of Australians have changed, with financial independence now the nation’s most common aspiration, according to a new report.

Overview of the Federal Budget 2023 – 24

The following are all the links to the federal government's description of its 2023 Budget. At the bottom are the Budget Documents for those that love to get into the fine detail of a Budget.

2023 Federal Budget: Stronger foundations for a better future

‘Seeing our people through the hard times – and setting our country up for a better future’

“While Australia may have a lot coming at us – we have a lot going for us too” – Dr Jim Chalmers, 2023-2024 Federal Budget Speech.

Our investment and economic forecasts, April 2023

Our latest forecast changes include expectations for:

The importance of SMSF succession planning

Preparing for loss of capacity or death is vital for SMSF members. It's important to ensure your trust deed is watertight.

ATO warns of rise in SMSF identity fraud and investment scams

The ATO has warned SMSF members to be aware of identity fraud and investment scams.

Banks launch scam awareness campaign

The new campaign highlights the importance of customer alertness against criminal activity by scammers.

Unintended consequences of work test changes to be rectified

New draft legislation to the work test mean impacted individuals will retain their ability to claim deductions for personal contributions post 30 June 2022, says a leading adviser.

Preparing for EOFY tax scams with business and cyber resilience

Every end of financial year (EOFY) season involves a rush by Australians wanting to get their tax returns completed. Increasingly, though, this period is seen as an opportunity for bad people to take advantage of us.

Legal Considerations Around Recording Customers Who Enter My Business

As a business, you may consider installing video surveillance on your premises to discourage theft or ensure the safety of your customers and personnel. However, your business may suffer significant legal implications if you do not adhere to legal requirements around filming or recording customers that enter your store.

Bank closures, market volatility call for perspective

Amid sudden bank closures, we explain our risk management approach and remind investors to focus on what they can control.

Weighing up cash deposits

Cash in a deposit account doesn't necessarily equate to safety. That's why many investors are shifting to fixed interest securities.

How Long Could You Survive Drinking Only ………

Here's how long you'd live consuming only this liquid, and nothing else.

More SMSF members accessing funds without meeting conditions: ATO

The ATO said it is seeing a rise in behaviours which indicate SMSF members may be accessing their funds before meeting the conditions of release.

More women take up SMSF as others look for advice

A new report from AUSIEX shows that in 2022, new SMSF trading accounts were relying more on advice, were increasingly female and favoured a distinct mix of asset classes, securities and sectors.

Devil in the detail on super changes

Proposed changes to superannuation have the potential to reshape the retirement landscape. The objective of super remains the missing ingredient in the mix.

Protect your business from cyber threats.

Computer hacking has been around for as long as there have been computers. Once it used to be computer geeks showing the world how smart they were. Now it's become very serious with almost any person, company or Government at risk from these criminal activities.

Australian retirees face accelerating price pressures

Couples now need nearly $70,000 per year to achieve a comfortable retirement, while singles need around $50,000 according to an analysis from the ASFA Retirement Standard.

Draft super objective to ‘protect super from interference’

Superannuation bodies have welcomed the government’s draft objective for superannuation, stating it will provide equity in the system and help protect preservation.

Three simple steps for financial wellness

If money’s too tight to mention, here’s some small steps that can make a big difference in achieving your financial goals.

Contribution caps to stay the same for 2023–24 year

Concessional and non-concessional contribution caps are set to stay at $27,500 and $110,000 following the release of the AWOTE figure.

Comparison: How Long It Takes To Decompose?

Check out how long everyday items take to decompose.

Why most investors want human advice

Artificial intelligence systems, and their ability to undertake often complex tasks in seconds, are increasingly gaining attention and user traction.

No plans to extend NALI compliance relief, says ATO

The ATO says it does not intend to extend PCG 2020/5 for another year and will wait to see what changes the government legislates.

China’s economic rebound lowers the odds of a global recession

Why markets are optimistic

Digital advice firm optimistic QAR will ‘reset financial advice’

Ignition Wealth says the final QAR report will help reshape advice and has pushed the government to implement the review’s recommendations in their entirety.

When to be proactive about your portfolio

The mid-year point is an opportune time to take stock of your investment holdings – but reviewing your portfolio should really be an ongoing exercise.

ATO warns SMSF on sole purpose test for property investment

Property investment by an SMSF will fail the sole purpose test if it provides pre-retirement benefit to someone such as personal use of a fund asset, warned the ATO director of the SMSF Auditors Segment.

TBC set for double indexation from 1 July

The general transfer balance cap is set to increase to $1.9 million from 1 July based on CPI figures released today.

Inflation edges lower while GDP grows but slows

The latest figures from the ABS reveal economic growth last year and show inflation coming off its peak.

Why superannuation fund fees matter

The fees you pay on your super could have a material impact on how you retire, which is why it's important to understand how they work.

One in seven SMSF directors yet to apply for ID

Around 100,000 SMSF directors still need to apply for their director ID despite the deadline passing two months ago. Extensions are available for legitimate reasons.

Australian equities retain grip on SMSF assets

The largest portion of the SMSF investment pool is held in domestic shares, according to a recent survey.

Beating back inflation, but at what cost?

Joe Davis, Vanguard’s global chief economist, gives a high-level overview of where the economy and markets are likely headed in 2023. Inflation is abating, thanks in part to central banks’ aggressive actions, but it may come at a cost, with recession likely in most developed markets. But it may not be all bad news for the financial markets.

ATO issues fresh warning on illegal early access schemes

With illegal early access schemes on the rise, the Tax Office has issued a fact sheet warning super members about the promoters of these schemes.

A review of the last two decades in investing

Robin Bowerman, Head of Corporate Affairs and Editor of Smart Investing, is retiring after almost 20 years with Vanguard. Here he reflects on the investment landscape over the last two decades.

Auditor flags surprising traps with e-signatures and SMSFs

A specialist auditor has explained some of the grey areas and confusing aspects of electronic signatures and SMSF documents.

ATO plans publicity campaign for final Work From Home guidance

More demanding record-keeping requirements in the November draft have been in place since 1 January.

Transitioning into retirement: What you should know

Deciding on your retirement funding options in retirement comes down to what makes the most sense for you.Deciding on your retirement funding options in retirement comes down to what makes the most sense for you.

An ongoing debate every employer needs to be on top of.

How to work it out: employee or contractor

To check if your worker is an employee or contractor, you need to review the whole working arrangement. Read on ….

Auditor flags knowledge gaps with loans and financial assistance amongst SMSFs.

Loans to members and financial assistance continues to be the most commonly reported type of contravention based on ATO statistics.

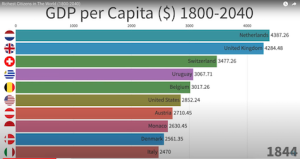

Countries with the highest GDP per capita between 1800-2040

check out 240 years of countries with the highest GDPs per capita

SMSFs cautioned on ‘strict conditions’ with SMSF lending

Where SMSFs are planning to lend money there are some important conditions to be aware of including who the money is lent to and the reason for the loan.

Downsizer age reduction now in force

With the eligibility age for downsizer contributions now age 55, the SMSF Association has highlighted some important considerations for younger clients looking to use the measure.

ATO raises alarm on asset protection scheme for SMSFs

The ATO is concerned about SMSFs entering into certain asset protection arrangements that involve a ‘Vestey Trust’.

2022 by the numbers

How did share markets around the world performed last year? And what investment lessons can we learn from 2022? Read on to find out.

Draft legislation released for franking credit changes

The government has released draft legislation on its measure to alter the tax treatment of off-market share buybacks.

Advisers warned on major timing traps with lifetime CGT cap

Planning ahead is critical for clients wanting to make super contributions under the lifetime CGT cap given some of the tight timeframes, CFS has cautioned.

Positive results from research into the value of financial advice.

A recent study shows that Australians who have an active relationship with a financial planner are not only better off financially than unadvised Australians – they also have a better quality of life.

SMSF professionals play critical role in Age Pension planning

With the recent ATO statistics indicating a significant proportion of SMSF members in retirement phase may be eligible for the Age Pension, Accurium has highlighted this as an important planning consideration.

Making the most of your super limits

Getting more money into superannuation is a proven way of building wealth to spend in retirement.

Three things to consider when switching your super

Understanding how your super works and making sure you are getting the most out of your fund is essential to achieving the retirement lifestyle you envision.

Volatility is here to stay

Volatility is part and parcel of investing so it's important to put it into perspective and look at the full picture when thinking about your wealth, rather than focus on day-to-day market swings.

A 2022 Advent Calendar for our clients

Come back each day and click on the next date for more inspirational and Christmas quotes.

ASIC consulting on changes to SMSF advice guidance

The corporate regulator is in the process of amending information sheet 205 and 206.

Rapid interest rate rises reveal global market frailties

Elevated volatility is a key feature of markets today.

By Jumana Saleheen, Vanguard Chief Economist, Europe

Investors and recessions

Despite much talk of rising interest rates and possible recession, here are a few reasons to stay the course and stick to your long-term investment strategy.

By Alexis Gray, Senior Economist, Vanguard Asia-Pacific

ATO raises ‘illegal early access’ concerns with small business owners

Recent research by the ATO has revealed a higher proportion of loans to members and non-lodgements among SMSF members with links to small business.

Federal Budget 2022/23 – Documents and Facts Sheets

All the detail for those who like to better understand the fine print.

Federal Budget 2022 — Winners and Losers

After 10 years out of government, Treasurer Jim Chalmers has delivered Labor's first budget since its election victory in May.

Federal Budget: all the key points you need to know

A rundown of the main measures that will impact accountants and small business.

Budget October 2022-23 – Comprehensive summary

The Federal Government is to continue spending more than it earns for at least the next two years at least.

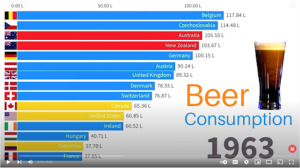

The Countries that Consume the Most Beer in the World

Check out the countries that consume the most beer from 1963-2021

Partial property sales eligible for downsizer

Superannuation fund members making a downsizer contribution do not have to sell the whole property or even move out of it after the sale, but cannot claim a contribution for land that has undergone a subdivision, a technical expert has advised.

The advantages of investing early

You may have heard it said, “No risk, no reward.” But did you know that time can actually decrease your risk while increasing your reward?

ATO provides cyber security tips for SMSFs

In the wake of the recent Optus cyber attack, the ATO and Australian Cyber Security Centre has outlined some important steps to help trustees keep their data safe.

Four powerful ways to build investing confidence

Here are some tips that can help you build confidence in your investing approach, no matter what the markets are doing.

Take action on valuations now to avoid delays, says ATO

The ATO is urging SMSFs to get their asset valuations done before their annual audit to help avoid delays and late lodgements.

How costs can add up

There is quite a bit of truth to the old adage “there is no free lunch in life” or its more recent equivalent “if you’re not paying for the product, you’re the product” because pretty much everything in life comes at a cost these days.

ATO taking ‘harsher’ stance on loans to members

The ATO is paying closer attention to attempts by accountants to “patch up” mistakes by SMSF clients involving the removal of money from the fund.

How much money do I need to retire?

When I retire, will I have enough money to enjoy the retirement lifestyle I envision? It's a question many of us will need to ponder at one point.

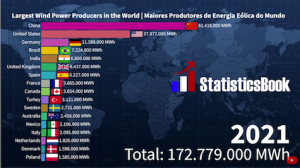

Largest wind power producers in the world

Check out the worlds largest wind power producers from 1990 to 2021

Bear Markets and What Investors Can Do Now

Six biggest bull markets in US stocks/shares since 1962 and their subsequent bear markets.

Proof of ownership flagged as ‘biggest’ crypto issue for SMSFs

SMSFs have been warned on some of the challenges in proving ownership of crypto assets, with only certain exchanges allowing SMSF accounts to be registered.

Claiming a tax deduction for expenses for a home-based business

If you operate some or all of your business from your home, you may be able to claim tax deductions.

Super changes apply, don’t get caught short

To avoid additional costs (including the superannuation guarantee charge (SGC)), you must pay the right amount of super for all your eligible employees by the quarterly due date.

A retirement plan built to last

Staying the course, and not being distracted by short-term market events, is just as important in retirement as it is at any other time.

Cyber Security – Optus data breach

In light of the recent Optus data breach, we thought it timely to provide a list of things you should consider to help protect your identity

Withdrawal strategies before death require careful consideration

Professionals have been warned there is a “fine line” between member benefits and death benefits where a member plans to withdraw shortly before death.

Pensions to face tougher scrutiny under new TBAR system

The move to the new quarterly based TBAR regime may see a clampdown on the backdating of pension documents, CFS has cautioned.

ATO clarifies critical reporting deadline with TBAR transition

The ATO has clarified that SMSFs will need to report all unreported events from the 2022–23 year by 28 October 2023 once the new framework starts.

Three tips for building a good portfolio

The first step to building a sound investment portfolio is to know why you’re investing

Strategic asset allocation: a timeless solution

While adopting a tactical asset allocation might seem tempting during bouts of heightened volatility, the timing and skill required to perfectly execute a portfolio shift is near impossible. Sticking to a strategic asset allocation however is likely to yield better returns.

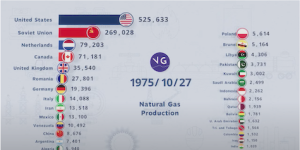

Largest natural gas produces by country from 1970-2021

See which country lead the worlds natural gas production at certain times in the last 50 years.

Preparing your kids for financial success

Teaching kids to establish sound money management skills and strong financial acumen is important, regardless of wealth level.

NALI ‘not going away anytime soon’

SMSF trustees have been urged to start reviewing any potential non-arm’s length expense issues with the outcome of any future government consultation still unclear at this stage.

A trio of trip-wires businesses should avoid, says ATO

Wayward habits accentuated by the pandemic will be a compliance focus.

Tax Office homing in property deductions, SMSFs warned

With property deductions a big focus for the ATO this tax time, SMSFs have been warned on some of the pitfalls in this area that can land them in trouble.

Documentation key in preventing ‘disappearing crypto’, SMSFs told

Thorough documentation can help mitigate the risk of crypto assets going missing in situations like divorce, says a specialist lawyer.

Should you be getting advice?

From navigating market volatility to superannuation legislation changes to determining the right asset allocation, here's how financial advice can help investors optimise their portfolios.

SMSFs warned on common mistakes with bare trusts

A specialist law firm has highlighted the importance of ensuring that the bare trust has been set up correctly where SMSFs are looking to borrow money.

How much time and money do you need to consider investing

There's a common misperception that in order to start investing, you need a large initial sum and lots of time. Here's why that's a myth.

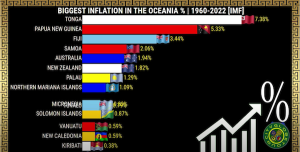

Largest inflation rates by country in oceania

See how the inflation rates changed from 1960-2022

How diversification fights investor biases

Investing in familiar names may bring a sense of comfort but by focusing too heavily on the Australian market, investors may limit their opportunity set and forgo the benefits of greater diversification.

Census 2021 Data

Search through the data collected by the Australian Bureau of Statistics, and find interesting facts about how the country is changing.

ATO statistics show 12 per cent jump in SMSF assets

The total value of SMSF assets has climbed to $892 billion during the 12 months to March, according to the latest ATO statistics.

ATO responds to GST case involving SMSF

The ATO has issued a decision impact statement on a recent decision that determined whether an SMSF was liable for GST on the sale of subdivided lots.

Tax tips

The more detail you can give your accountant the quicker your tax return can be processed and, usually, the better the outcome. The following will help.

Super Contribution Changes starting 1 July 2022

From 1 July 2022, there will be changes made to super to make it easier for Australians to grow their retirement savings.

Using trusts: Keeping it in the family

Trusts are used to hold assets for various reasons, but most typically for tax planning and asset protection purposes. Here's a little more insight into how trusts work.

Work test changes open up TBC strategies for couples

The contribution changes coming in on 1 July will provide more time for spouses in SMSFs to even up their balances and maximise their transfer balance cap, according to an advisory firm.

RBA rate rise spurs mixed response from SMSF lenders

While the official interest rate increase has seen some SMSF lenders raise their interest rates, others are holding off for now.

ATO flags changes to TBAR reporting

New rules are in effect, which will see changes to how SMSFs manage transfer balance lodgement.

Make the most of these super opportunities before June 30

With only about four weeks left until the end of this financial year, now's a good time to check your superannuation options.

Talking money with a partner

Here are some factors to consider before you join finances with a partner.

How advice gets you closer to your goals

A recent Vanguard survey found that investors believed financial advice provides substantial portfolio, financial and emotional value, and got them closer to achieving their financial goals.

Weighing up value and growth

What's the difference between value and growth investing, and how can you incorporate these investment factors into your portfolio?

Investors are becoming more ethically conscious

Investors worldwide are becoming more actively engaged with where their money is being invested, with flows into ESG products continuing to build momentum.

Largest cities in the world 1500 to 2100

The information in this chart is fascinating from both an historical perspective as well as what it predicts. It also guarantees you'll be the breakfast table expert every time.

ATO ruling may offer solution to NALE issues

Amendments being made to contribution ruling TR 2010/1 may provide a fix to some of the significant issues with the non-arm’s length expenditure rules, said the SMSF Association.

ATO ramps up identity fraud detection for new SMSFs

Around a quarter of the individuals being identified as high risk under the ATO’s new registrant program have compromised identities, said the ATO.

SMSF account openings shift from self-directed to advised clients

The statistics have begun to change coming out of the COVID-19 pandemic, according to new findings from Australian Investment Exchange Limited (AUSIEX).

SMSFs warned on NALE uncertainty

Heffron says SMSFs still need to be cautious around non-arm’s length arrangements.

Where self-managed super funds are investing

Recently released ATO data shows some SMSFs have too much of their money invested into just a few asset classes and are not as diversified as they could be. Here's why having broad market exposure is important in retirement.

Investing for a house deposit

Despite it seeming increasingly difficult to get on the property ladder, there are still a few ways younger investors can realistically work towards a house deposit.

Constructing a portfolio using investor profiles

Vanguard research showed that not all younger investors had a high equity allocation and not all older investors reduced risk as they aged. Consider constructing a portfolio using diversified funds that not only considers your investment time frame, but also aligns to your attitude towards risk.